Some issues and concepts come up frequently, so the notes here focus on some practical over theoretical or technical points to consider.

Thought: Consider the Federal Reserve Bank’s largest member banks (its owners) print more imaginary ‘money’ through derivatives than the Federal Reserve Bank’s “quantitative easing”. The Federal Reserve Bank’s “QE” prints in the ballpark of $20 trillion from out of nowhere into existence but the Federal Reserve’s owners print over $1,000 trillion fictional money in the form of derivatives not yet brought into existence. This derivation of ‘money’ not in existence, most in the form of interest rate derivatives is a mechanism that can control the interest rate structure (at least short-term) i.e. the cost of capital in the ‘real’ world.

- Inflation

- Deflation

- Derivatives

- Federal Reserve Bank (System)

- Federal Reserve 0% Interest Rate, “ZIRP”

- Mortgage Securitization

Inflation:

Inflation is simply the expansion of the money supply. Inflation is the printing of dollars by the Federal Reserve beyond the capacity of the economy to earn them through the production of goods and services, because the Federal Reserve does not have this money. Inflation is not a rise in price levels, although rising prices can be a symptom of inflation because there are different reasons why prices rise, i.e., changes in demand and supply. Inflation or printing money is the silent factor – the third wheel – that can distort supply and demand.

The term currency devaluation would scare most people, so it is called ‘inflation’. A $50 loaf of bread or a $100 trillion Zimbabwe note is not due to increased demand, but inflation or devalued currency. When the Federal Reserve speaks about inflation, it is for practical purposes, getting at a quiet or soft devaluation through the printing or ‘inflation’ of currency.

Printed money finds its way into raising the cost structure of production and increased costs for consumers. Subtle signs that mask unofficial currency devaluation through inflation may be seen in the reduction of quantity, size, or lowered quality of a product but charged at the same or higher prices on basic commodities or staples such as sugar, wheat, rice, fuel, etc. Food and energy prices tend to rise quickly as devaluation through inflation accelerates, although U.S. consumers spend among the lowest percentage of their income on food and energy compared to the rest of the world.

The effects of inflation are not isolated in the U.S. but can have greater destabilizing effects on other countries where people spend a significant percentage of their income on food such as India, many countries in Africa, the Middle East. The idea is the printed money, the ‘liquidity’ makes it way into the commodities market (world trade for basic raw materials such as agricultural products, fuel, etc.) and pushes up prices with ‘inflated’ dollars and forces higher prices across the world.

Many countries have been engaged in what is called ‘currency wars’ to devalue its own currency by printing money. Perhaps a difference is some do it from a position of strength (maintain competitive trade) as others from a position of weakness (to pay debt) or some weighting of both. So there are a few faces to inflation or devaluation through printing money: pay debt because production alone can not do it, maintain an edge in trade, indirect war to cripple countries most affected by certain types of inflation, etc.

The U.S. had an official devaluation of the dollar against gold in 1933 under President Roosevelt and in 1971 under President Nixon when too many dollars had been printed against the gold supply at the given price, and other nations were no longer allowed to redeem their U.S. dollars for gold.

And no, rising prices are not due to melting polar ice caps (although the largest banks have a derivatives market on standby to save the world from either global warming or cooling, as they provided for housing. CBO had done extensive work on cap and trade, a derivatives market for the trading emissions allowances; Goldman Sachs is on CBO’s panel of economic advisors to perhaps help navigate the complex world of derivatives.).

The increasing number of dollars to buy gold signals this inflation-unofficial dollar devaluation. At the crux of it is loss of confidence. That is why central banks printing money fear this metal and why other countries, such as Germany, are scrambling to count their gold bars being held at the Federal Reserve Bank of New York. Unlike mortgages, there can not possibly be multiple claims on that gold. Actually, it is rather blasphemy for Ph.D. economists to speak about gold, as the Federal Reserve has a corridor connected to choice economics departments and its partnership can be helpful in publications and tenure.

Deflation:

Just as inflation is not a rise in prices, deflation is not a decline in prices, although rising-falling price levels can be symptoms of inflation-deflation, respectively, because there are different reasons why prices rise or fall.For instance, the price of a flat screen TV or laptop computer has fallen significantly over time. The fact that these prices have fallen is not deflation but is a result of free market interaction among demand and supply, greater technological efficiencies and competition that lower prices.

In the current environment, a practical term for deflation is “asset collapse,” a term rather absent from the media and Federal Reserve Bank announcements since the banking and financial system collapse in 2008. As asset prices collapse, the Federal Reserve Bank prints or ‘inflates’ massive amounts of money it does not have to prevent the asset collapse in its member banks and financial institutions (because their failure will ignite the OTC derivatives on and off their balance sheets).

Prices of commodities – what people “need” to live such as agricultural products, fuel, energy (‘commodities’, basic raw materials) rise due to the “inflated” printed money (see inflation). Gold (with it silver) rises as a “radioactive” detector of monetary expansion (printing money) beyond the productive capacity of the economy. That is, inflation-deflation are monetary phenomenon.

Derivatives:

A derivative is a legal financial contract between two parties, where the value of the contract is ‘derived’ from or based on the underlying value of an asset(s) and its changes. There are different types of derivatives, and a general distinction is whether derivatives are traded in a transparent market such as an exchange, or an opaque and unregulated market.

To illustrate, most people have what is akin to a derivative contract, such as car or home insurance. An insurer assesses the value of the car or house, the risks of the driver or homeowner, etc. and offers the owner an insurance rate based on those factors. Policy holders pay periodic insurance premiums to the insurer, and in the event the car or house is damaged-destroyed, the insurer pays the holder the value of the car or house at that point. This transaction can be thought of as an ‘exchange-traded’ derivative where it is transparent, known who has contracted with whom.

The worst banking and financial collapse in a century or few since 2007/2008 that is still unfolding came privately-traded derivative transactions known as Over-the-Counter (OTC) derivatives. These were the mortgage bonds (MBS/CDO/CMO/ABS) securitized by the underlying value of the mortgage payments and home value, and another type of derivative called credit default swaps (CDSs) ‘insurance’ wrapped around the MBS derivative. Unbeknownst to most homeowners, the largest banks and financial institutions could take out or wrote 5 or 10 different CDS ‘insurance’ policies on the same house or on the insurers themselves. In the case of default, the losses became exponential.

With OTC derivatives, it is not known who has contracted with whom and the counterparty risks involved as the contracts are privately transacted and there is no central repository of information on the contracts and its counterparties. There are over $1,000 trillion of these among the largest banks and financial institutions without the assets or capital to back them up.

Some have called this a “casino.” Granted, I am unfamiliar with casinos and gambling, but it is my understanding that casinos at least require a credit line or actual collateral before large bets are made. That is not the case with the amount of OTC derivatives outstanding.

Federal Reserve Bank:

The Federal Reserve Bank became the central bank for the United States through a Congressional charter in 1913 that gave the Federal Reserve Bank the power to create or print money and control over the nation’s money supply through its monetary policy. Its stated mandate is to maintain maximum employment, stable prices and long-term interest rates and so on.This is the Federal Reserve’s public component.

The Federal Reserve Bank also has a private component, even though most people, including Ph.D. graduates of economics, understand the Federal Reserve to be purely a government entity and the Federal Reserve presents itself as such:

While the Federal Reserve System is not owned by anyone, the Federal Reserve Bank is comprised of a conglomerate or group of banks, the most important being the largest banks in the country that are for-profit and “shareholders” (that would mean ownership to many) of the system; the largest banks do not return their profits to the public Treasury. One of the prominent early founders of the Federal Reserve Bank was JP Morgan, currently the largest bank bearing his name in the U.S. The quasi-private nature of the Federal Reserve Bank is its mix of public and private interests, although the Federal Reserve emphasizes its public role.

Banks that are national are member banks of the Federal Reserve System as other banks apply for membership. The largest member banks of the Federal Reserve System by asset size include JP Morgan Chase, Bank of America, Citigroup, Wells Fargo, Goldman Sachs, and Morgan Stanley that hold north of three-quarters of the nation’s banking assets.

Of the twelve districts that make up the Federal Reserve System around the country, the Federal Reserve Bank of New York is considered to be the most powerful. The NY FRB member banks can be found here, as can a visit to the other districts to see other member banks.

The authority on the Federal Reserve Bank is G. Edward Griffin, author of The Creature from Jekyll Island, which documents the origins and creation of the Federal Reserve. There are many videos of his lectures on the Federal Reserve on YouTube.

Mortgage securitization:

It is not uncommon for homeowners to think their mortgage payments end at the bank, their lender. For the majority of home mortgage loans (and other types of loans) it is only the beginning of the process where their mortgages could end up being owned by a mutual fund, pension fund, 401k, or investors in Europe or Asia.

Some important concepts in securitization are that the ownership of the mortgage, which is originally the bank or lender, can be sold by the lender (bank) to another party such as Fannie Mae or Fannie Mac; it was not uncommon for the mortgage to change hands multiple times. Also, think of the house as the collateral or the “security” behind the homeowner’s mortgage, which can be foreclosed upon should the homeowner default or stops making mortgage payments.

Here is a general description of what happens after homeowners sign the mortgage documents:

The banks sell the majority of the home mortgage loans to Fannie Mae or Freddie Mac.In selling the mortgage, an important concept is that the risk of loan default is transferred from the bank to Fannie Mae and Freddie Mac. The banks often retain what is called the servicing rights to ‘service’ the loan, meaning to collect the mortgage payments, insurance premiums, escrow, etc. The banks make money throughout the process including (1) originating the loan, i.e. lending the homeowner the money, (2) in selling it to Fannie Mae or Freddie Mac or to other banks, and (3) in the servicing fees. A bank may have started out as the homeowner’s lender, but may end up being the servicer after it sells the loan.

Fannie Mae and Freddie Mac gather up say, 500 to 1,000 similar mortgages and “securitizes” or pools them together to create what can be thought of as a mutual fund filled with mortgage payments. This is called a mortgage bond or a mortgage-backed security (MBS), because these MBSs are ‘backed’ or collateralized by the debt of homeowner’s mortgage payments. Other terms are CDOs (collateralized debt obligations), CMOs (collateralized mortgage obligations), ABSs (asset-backed securities).

Fannie Mae and Freddie Mac “issues” or sells MBSs, which are referred to as agency bonds or agency MBSs, to investors and guarantees the investors the homeowners’ timely payment of the principal and interest payment. The largest banks also securitize mortgages and issue their own MBSs, which are called private label MBSs that they sell to investors.

Investors, such as pension funds or other mutual funds, buy or invest in MBSs as these mortgage bonds offer a steady “fixed” return from the interest on the mortgages in the MBS, for example, say 5% and the homeowner’s payment of principal.

The investors then become the homeowners’ ‘lender’, i.e. the owner of the homeowner’s mortgage payment. Homeowners are really sending money to the bank to ‘service’ or process the payments and sends it off to the investor.

Federal Reserve’s 0%, Zero-Interest Rate Policy (“ZIRP”):

Sincethe banking and financial system crisis-collapse in 2008, the Federal Reserve has targeted the (short term federal funds) interest rate near 0% for its member banks. In practical terms, this means member banks of the Federal Reserve pay close to 0% to borrow and lend that money to the public at say, 4% or 5% or 8% for home, business or student loans, or make even more in the stock market (that’s where bank profits came from). Or, the banks also use that money to stockpile U.S. Treasury bonds as its remaining few buyers and be paid by taxpayers to hold them to keep banks above the Black Hole as shown in my post, the Federal Reserve’s Love Affair….

ZIRP in the real economy signals deep trouble. ZIRP destroys peoples’ savings by paying them 0% – the savings that form the pool of capital from which businesses can draw upon to create jobs. This is akin to saying that savings earned from years of hard work is no different than money printed at will.

Very little attention, if any, is given to how destructive ZIRP can be to producers-employers. Devalued dollars-printed money-inflation means producers will pay more dollars to purchase inputs, i.e. raw materials and parts for production, thereby raising the cost structure for firms. Producers can only pass a portion of these costs to consumers who are indebted, underwater on their homes, have had savings erased or jobs lost. Producers are forced to raise prices, cut employees, reduce wages to make a profit or shut down. Devalued dollars may help producers export as some argue, assuming jobs have not been shipped abroad, for instance, 35 of the largest U.S. multinational companies added nearly 3 times more jobs abroad than they did in the states, as per capita income grows in Asia and falls in the U.S.

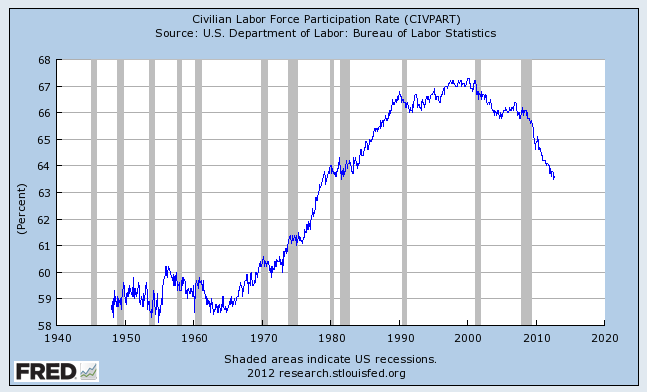

That is why it seems counter-intuitive that prices continue to rise as real incomes shrink, demand falls and the average family net worth falls by 40% after 2008. The U.S labor force participation rate – the percent of people in the workforce – has been set back 30 years and tells the long-term picture of the housing market, assuming an income is needed to buy a house despite historically low interest rates.That is a sample of the effects of currency devaluation, aka, inflation, aka, printing money and ZIRP reverberating through the economy and the on-going consequences of trillions in derivatives that collapsed the market and economy in 2008.

{kind=link}